2nd June 2025

Hosur Road is evolving into a premium residential hub, driven by the Yellow Line Metro and rising Grade A developments. Thus, the market is set for 15–20% annual price growth and a sharp rise in end-user demand for the next 2-3 years.

The Hosur Road micro-market in South Bengaluru, encompassing the Electronic City IT hub and Jigani-Bommasandra industrial zone, has remained a hub for blue chip companies such as Infosys, Wipro, TCS, HCL, Tech Mahindra, Bosch, and Biocon. This corporate presence has consistently attracted a large workforce, triggering sustained housing demand in the region.

An improved infrastructure developments such as the Electronic City Elevated Expressway and NICE Road have significantly enhanced connectivity to major parts of Bengaluru. As a result, Hosur Road has rapidly evolved into one of the city’s most sought-after residential corridors. The upcoming Namma Metro Yellow Line (RV Road to Bommasandra)—now in its final phase of construction and slated for full operation by Q4 2025—is expected to further catalyse residential growth.

Notably, the region has experienced a strategic shift in recent years—from a predominantly mid-income housing market to an emerging premium segment. The advent of the Yellow Line has triggered heightened interest from Grade A developers, transforming the area from an investor-driven market to one that increasingly appeals to end-users.

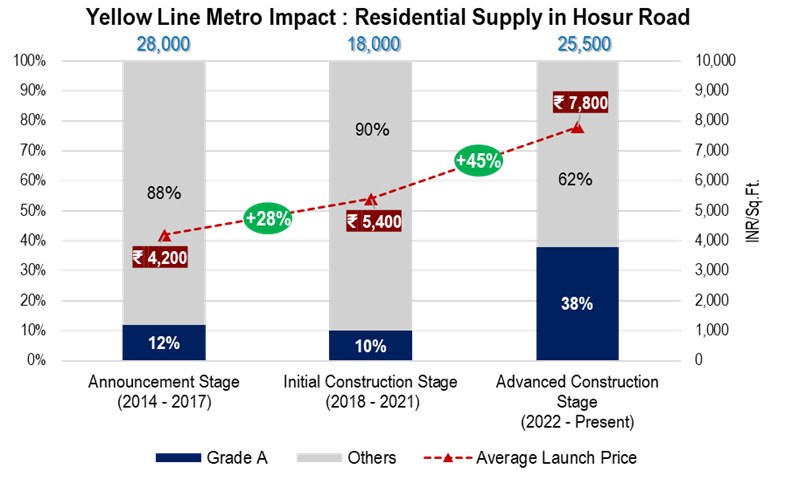

This blog decodes the “Yellow Line Metro Effect”, tracking the evolution of Hosur Road’s residential landscape from the initial announcement to the current advanced construction stage, while offering a forward-looking outlook post metro operation.

Overall, the construction of the Yellow Line Metro has significantly enhanced the appeal of Hosur Road micro-market for end users. The area is undergoing a transformation from mid-segment to premium segment market. During the advanced construction stage, the share of Grade A supply tripled, and average annual absorption increased by ~35%.

The growing demand for larger, more premium homes has resulted in:

With the Yellow Line Metro operations expected by Q4 2025, the Hosur Road residential market is poised for further evolution. Based on trends observed in similar metro-influenced corridors like Kanakapura Road and Mysore Road, the following trends are anticipated in the 2025 -2027 period:

Building Plan Approval process in Bengaluru Metropolitan Region (BMR)

How well do you know the statutory authorities related to real estate developments in Hyderabad Metro?

Check your understanding regarding Building Plan Approval process in Chennai Metropolitan Area (CMA)

How well do you know the statutory authorities related to real estate developments in Chennai Metropolitan Area (CMA), take this short quiz to find out.

Check your understanding regarding Building Plan Approval process in Hyderabad Metropolitan Region

A lot of architectural and interior design knowledge is required to make informed decisions while designing a co-living workspace. Take this short quiz to find out if you are ready!

Do you know it all that is required to make you successful in co-living industry space? Take this quick short quiz to grade your knowledge of the Co-Living market in India.

Take this short quiz to gauge your understanding the concept of re-purposing!

How well do you know the statutory authorities related to real estate developments in Bengaluru Metropolitan Region? Take this Quiz to find out!