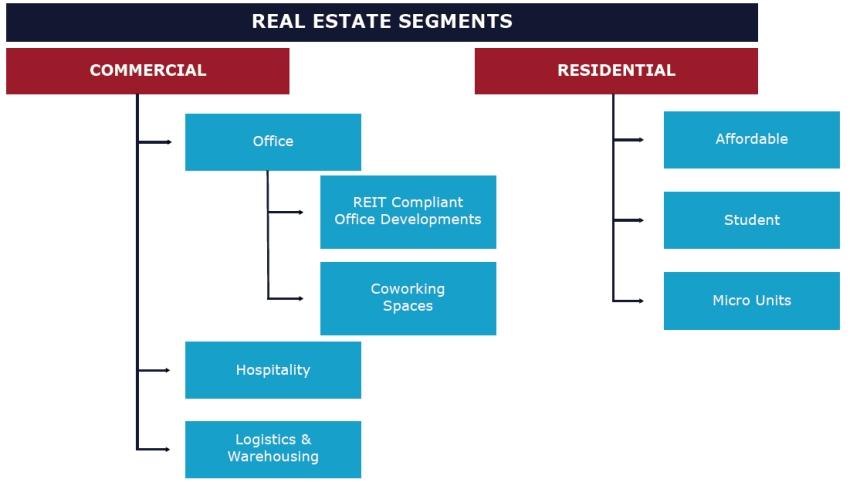

Opportunities in traditional real estate segment will remain, however, newer segments will witness increased interests and investments on account of huge untapped demand.

| OPPORTUNITY IN COMMERCIAL SEGMENT |

| Segment |

REIT Compliant Developments |

| Target Segment |

Value of assets not less than INR 500 Cr. Value of assets not less than INR 500 Cr.- Not less than 51% of value of the assets shall be rent generating.

|

|

Bangalore |

Chennai |

Hyderabad |

| Current Market Scenario |

86.2 million sqft (52%) of office stock is eligible for REIT listing. |

27.2 million sqft (41%) of office stock is eligible for REIT listing. |

28.4 million sqft (50%) of office stock is eligible for REIT listing. |

| Why Opportunity? |

- REITs can be floated even for a single asset project.

- Five smaller developers can pool their revenue earning Grade A office developments for REIT listing.

- REITs can be subscribed by foreign investors and raise debt capital by issuing debt securities.

|

| Key Locations |

Outer Ring Road, Whitefield & Bangalore North with high component of REIT eligible stock |

OMR |

HITECH City, Gachibowli |

| OPPORTUNITY IN COMMERCIAL SEGMENT |

| Segment |

Coworking |

| Target Segment |

- Start-ups & MSMEs with less than 50 employees, uncertain cash flow, growth and scale of operations

- Jobs with flexible work options & timings

- Transitional office requirements or where seats remains vacant due to stationing of employees at site locations.

|

|

Bangalore |

Chennai |

Hyderabad |

| Current Market Scenario |

1.4 million sqft of coworking space |

0.2 million sqft of coworking space |

0.3 million sqft of coworking space |

- Lower vacancy levels in office developments, high cost of leasing & lock in periods.

- Lesser availability of 1-10 seater workspaces in Grade A developments

|

| Why Opportunity? |

5.6 million sqft of additional coworking requirement by 2022

|

0.6 million sqft of additional coworking requirement by 2022

|

2.1 million sqft of additional coworking requirement by 2022

|

- Areas well connected & proximate to business districts

|

| Key Locations |

- CBD (MG Road, Residency Road), SBD (Koramangala, Inner Ring Road, Old Airport Road, Indiranagar, Old Madras Road), Outer Ring Road & Whitefield.

|

OMR, Guindy, Nugambakkam |

Hitech City, Gachibowli, Jubilee Hills, Kukatpally, Kondapur |

| OPPORTUNITY IN COMMERCIAL SEGMENT |

| Segment |

Hospitality |

|

Bangalore |

Chennai |

Hyderabad |

| Target Segment |

Business Travelers from IT/ITES sector |

Business Travelers & MICE |

Business Travelers from IT/ITES sector, MICE & Weddings |

| Current Market Scenario |

- 12,560 operational rooms.

- 65% Average Occupancy Rate

- 1 Job Attributes to 1.7 room nights.

|

- 8,732 operational rooms.

- 63% Average Occupancy Rate

- 1 Job Attributes to 1.0 room nights.

|

- 6,013 operational rooms.

- 64% Average Occupancy Rate

- 1 Job Attributes to 1.3 room nights.

|

| Why Opportunity? |

- 8,150 additional hotel room requirement by 2022

- 3,000 rooms under-construction and will meet only 37% of the addressable market.

|

- 4,516 additional hotel room requirement by 2022

- 600 rooms under-construction and will meet only 14% of the addressable market.

|

- 3,672 additional hotel room requirement by 2022

- 900 rooms under-construction and will meet only 24% of the addressable market.

|

| Key Locations |

- In proximity to the business districts like Whitefield, Outer Ring Road, Central and North Bangalore.

|

OMR, Mount Road, Egmore |

In proximity to the business districts like HITECH City, Gachibowli & Banjara Hills |

| Segment |

Logistics & Warehousing |

| Target Segment |

Industrial & Retail sectors are the key drivers |

|

Bangalore |

Chennai |

Hyderabad |

| Current Market Scenario |

- 17.7 million sqft of warehousing space.

|

10.9 million sqft of warehousing stock |

9.2 million sqft of warehousing stock |

| Why Opportunity? |

- 11.6 million sqft of additional warehousing requirement by 2022

- Can be developed on Agricultural & Green Land.

|

- 18.6 million sqft additional requirement of by 2022.

- Manufacturing Capital of India - Investments under Make In India Initiatives will propel industrial warehousing demand.

- Chennai & Ennore Port will facilitate ICD & CFS warehousing.

|

- 16.7 million sqft additional requirement of by 2022.

- Increased demand for warehousing in the e-commerce and retail space on being equidistant from the consumption hubs of Bangalore & Chennai.

|

| Key Locations |

- Nelamangala-Dabaspet, NH 648 (near Chikka Thirupati) & NH 75 (Hoskote – Narasapura belt)

|

Walajabad, Mappedu, Sunguvarchatram, Mannur on the Sriperumbudur-Oragadam-Maraimalai Nagar & Periyapalayam-Gummidipoondi clusters |

Medchal-Dandupally & Shamshabad, Kothur – Turkapally cluster |

| OPPORTUNITY IN RESIDENTIAL SEGMENT |

| Segment |

Affordable Housing |

| Target Segment |

- Households in the income bracket of INR 3 – 6 lakhs per annum.

- Constitutes 11%-15% of the urban households.

|

|

Bangalore |

Chennai |

Hyderabad |

| Current Market Scenario |

- Average annual demand of 9,000 units

- Only 15% of the addressable market is met.

|

- Average annual demand of 3,100 units

- Only 12% of the addressable market is met.

|

- Average annual demand of 4,400 units

- Only 4% of the addressable market is met.

|

| Why Opportunity? |

- 59,000 units additional requirement by 2022.

|

- 19,500 units additional requirement by 2022.

|

- 28,000 units additional requirement by 2022.

|

- Developer can avail benefits under PMAY’s Affordable Housing in Partnership.

|

| Key Locations |

- Bangalore North, Old Madras Road (Towards Hoskote), Tumkur Road, Mysore Road and Anekal – Jigani

|

OMR, Avadi, Oragadam, GST Road |

Miyapur, Shadnagar, Maheshwaram, Pocharam |

| OPPORTUNITY IN RESIDENTIAL SEGMENT |

| Segment |

Student Housing |

| Target Segment |

- Migrant student population in the age group of 18-23 years

|

|

Bangalore |

Chennai |

Hyderabad |

| Current Market Scenario |

- Latent demand for 36,100 beds.

- Only 5.8% of the addressable market is met by third party student housing facilities.

|

- Latent demand for 40,600 beds.

|

- Latent demand for 43,800 beds.

|

- Mainly provided by colleges and universities as campus hostels as well as by the unorganised sector.

- Available accommodation mostly provides minimal facilities at comparatively higher costs and lack of student centric layouts.

|

| Why Opportunity? |

- Average annual requirement of 13,800 beds during 2018-2022.

- Can be developed on Residential, Public & Semi-public zoned land.

|

- Average annual requirement of 5,000 beds during 2018-2022.

|

- Average annual requirement of 5,600 beds during 2018-2022.

|

| Locations |

- Within 2 kms/ walking distance of colleges and universities.

|

| OPPORTUNITY IN RESIDENTIAL SEGMENT |

| Segment |

Micro-Unit Housing |

| Target Segment |

- Households in income bracket of INR 6-10 Lakhs per annum with accessibility to home loans

|

|

Bangalore |

Chennai |

Hyderabad |

| Current Market Scenario |

- Average annual demand of 18,000 units; only 10% of the demand is met annually.

|

- Average annual demand of 12,500 units; only 6% of the demand is met annually.

|

- Average annual demand of 11,400 units; only 4% of the demand is met annually.

|

| Why Opportunity? |

- Average annual requirement of 22,500 micro-units during 2018- 2022.

|

- Average annual requirement of 15,500 micro-units during 2018- 2022.

|

- Average annual requirement of 14,500 micro-units during 2018- 2022.

|

- Benefit of 100% tax deduction on profit can be availed under PMAY’s Affordable Housing in Partnership.

|

| Locations |

- In proximity to IT economic hubs.

|

- Bangalore North, Electronics City, Sarjapur Road and Whitefield

|

- OMR, GST Road, Moggapair, Medavakkam, Velachery, Peramubur, Ambattur

|

- Gachibowli, Madhapur, Miyapur & Nizampet

|